What Is Ammonium Metatungstate (AMT)? The Complete Industry Guide (2026)

A professional breakdown of AMT’s chemistry, industrial applications, live pricing, market data, and the geopolitical forces reshaping global supply chains — updated March 2026.

What Is Ammonium Metatungstate (AMT)?

Walk into any modern oil refinery, glance at the smart glass darkening on a high-rise office building, or hold the smartphone in your hand — and you are looking at the downstream output of a white crystalline powder called Ammonium Metatungstate, or AMT.

AMT is an inorganic tungsten compound belonging to the polyoxometalate (POM) family. It is one of the most important homopolyacid salts of tungsten, with critical applications in petroleum refining, electronics, defense, aerospace, metallurgy, and anti-corrosive coatings.

As of March 2026, AMT sits at the epicenter of the most dramatic commodity supply crisis in the tungsten industry’s recent history, driven by China’s export restrictions and surging demand from defense, semiconductors, and clean energy sectors.

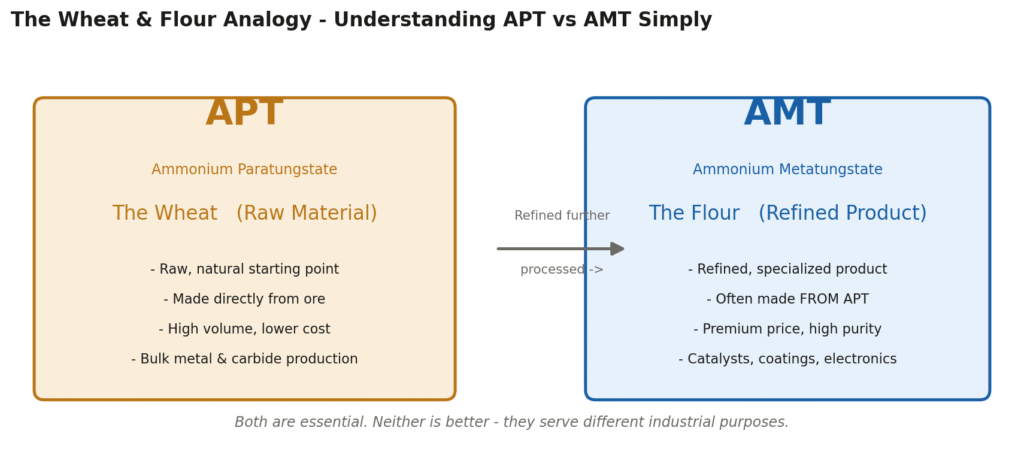

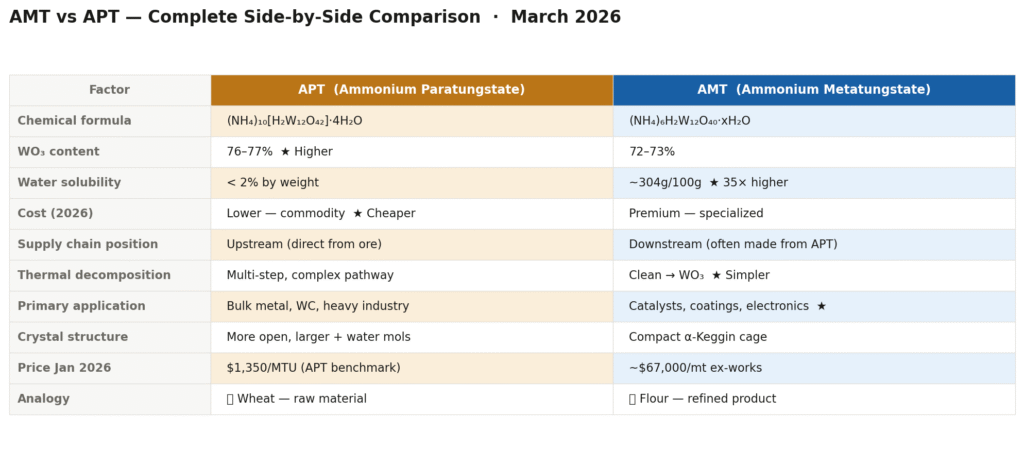

Simple analogy: If APT (Ammonium Paratungstate) is the wheat grain of the tungsten world — raw, natural, the starting point — then AMT is the refined flour. Processed further, more soluble, more specialized, and commanding a premium in global markets. → See our full AMT vs APT comparison in Section 8.

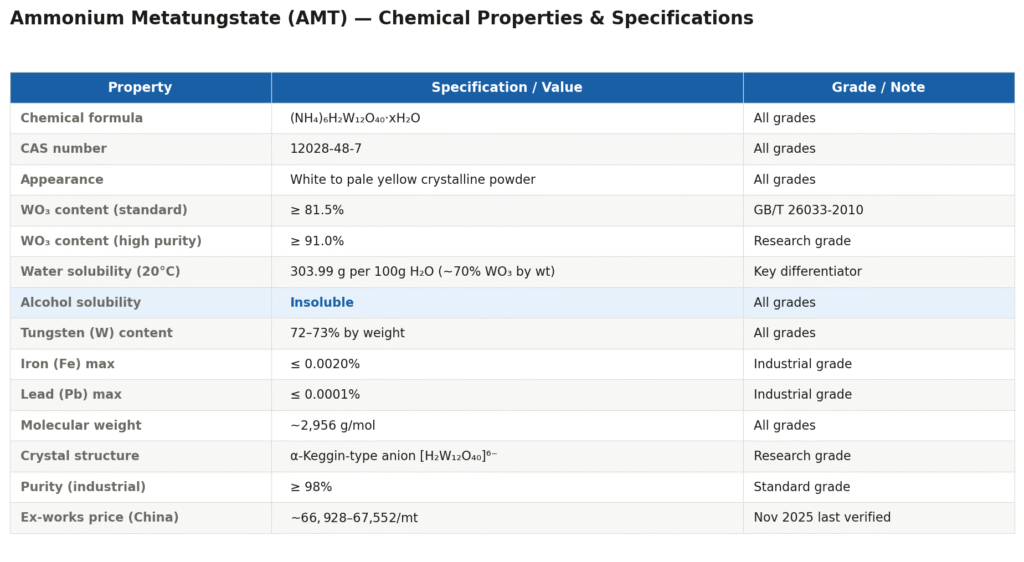

Chemical Properties & Specifications

Understanding AMT’s physical and chemical properties is essential for procurement, quality assurance, and process engineers working with tungsten intermediates.

The solubility advantage: AMT’s most commercially decisive property is its exceptional water solubility — approximately 35× higher than APT (which dissolves at under 2% by weight). This single property determines AMT’s entire industrial value proposition in catalyst preparation, thin-film deposition, and precision coating.

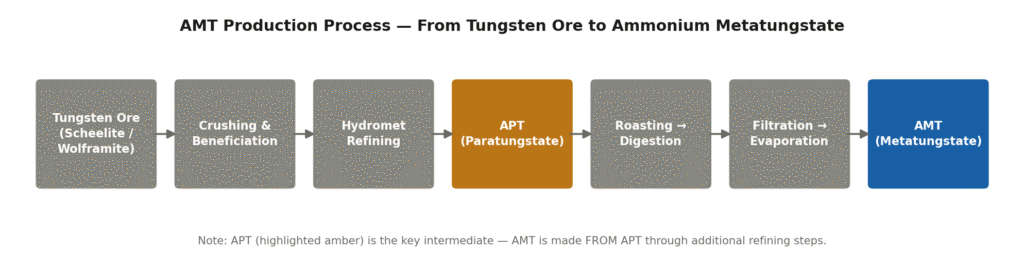

How AMT Is Manufactured

AMT sits downstream in the tungsten processing chain. Manufacturing starts with APT and requires several additional steps: roasting, digesting, filtering, evaporating, and spray drying.

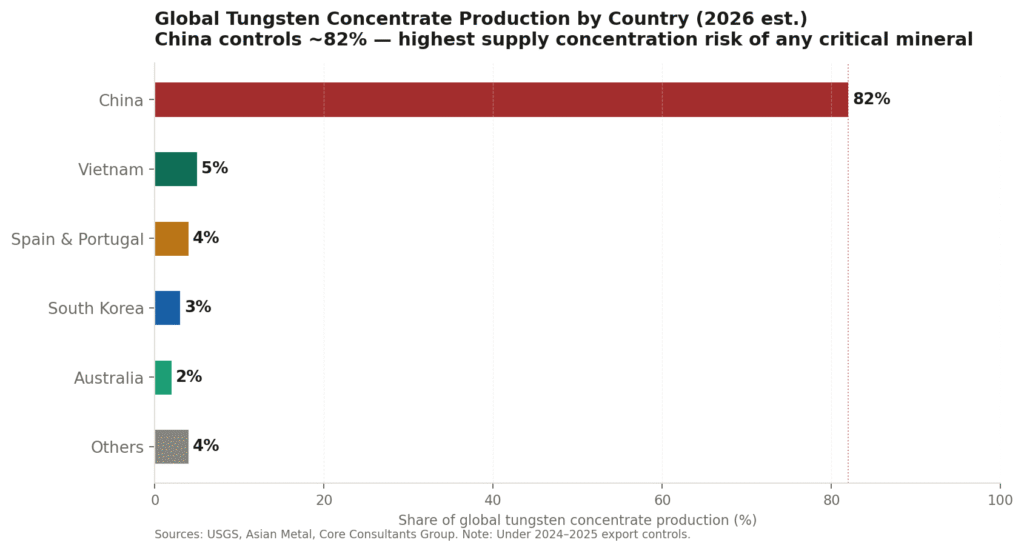

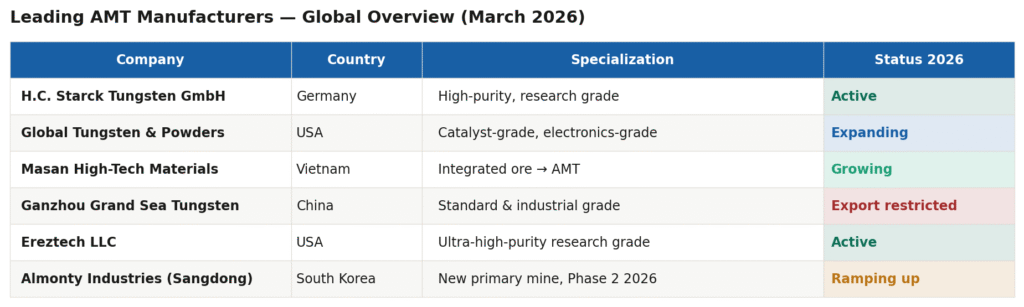

China accounts for over 80% of global tungsten concentrate production, with multiple facilities exceeding 10,000 metric tons per year of AMT output. Leading global producers include H.C. Starck Tungsten GmbH (Germany), Global Tungsten & Powders (US), Masan High-Tech Materials (Vietnam), and Ganzhou Grand Sea W & Mo Group (China).

Recent innovation: In February 2026, Global Tungsten & Powders launched AMT-Pro NextGen — a new grade optimized for high-pressure hydrocracking catalysts, achieving 15% improved solubility compared to legacy grades.

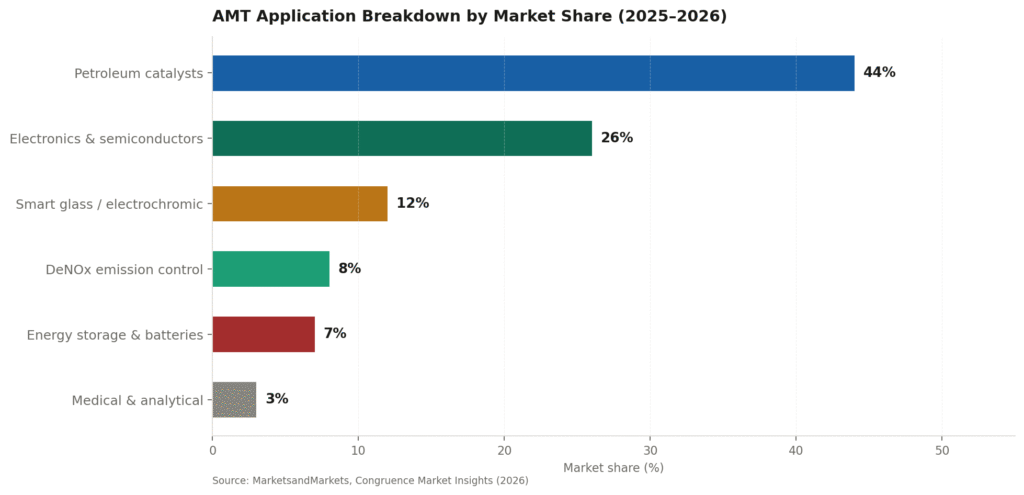

Where AMT Is Used — Applications & Market Share

AMT’s application base spans six major industrial segments, each leveraging its unique solubility and decomposition properties.

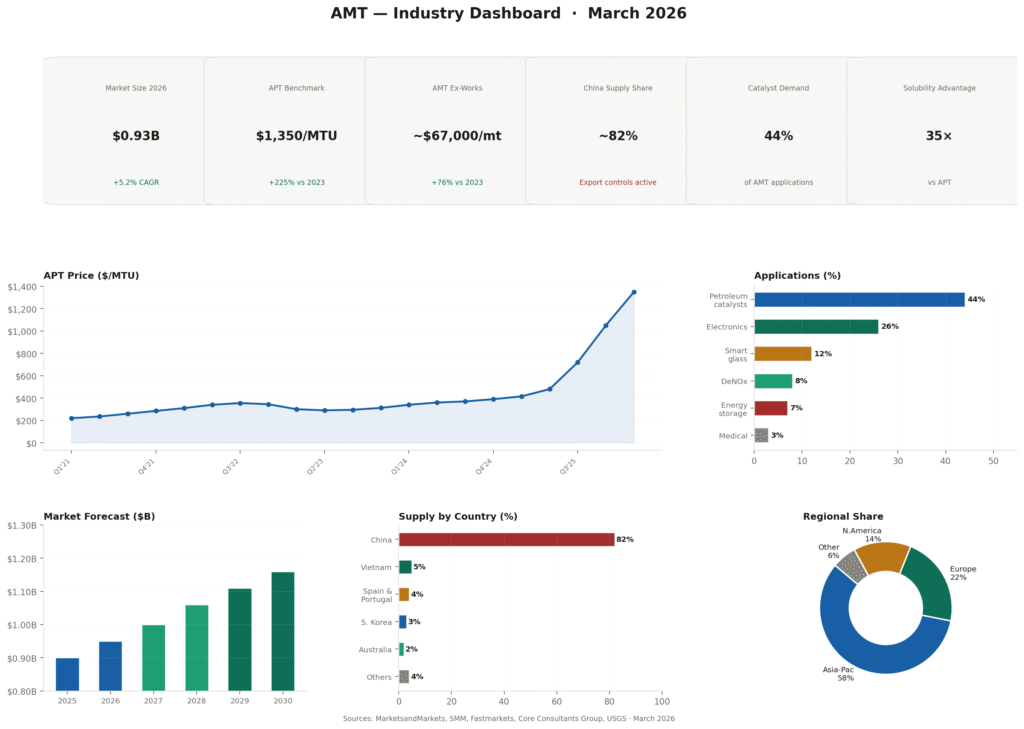

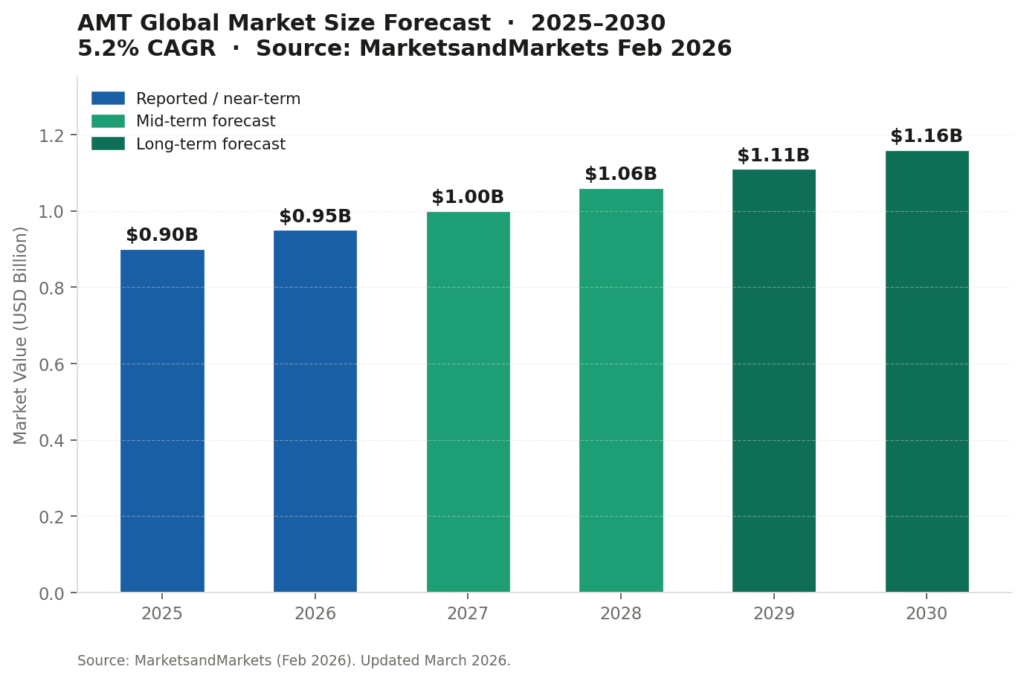

Live Pricing & Market Data (2026)

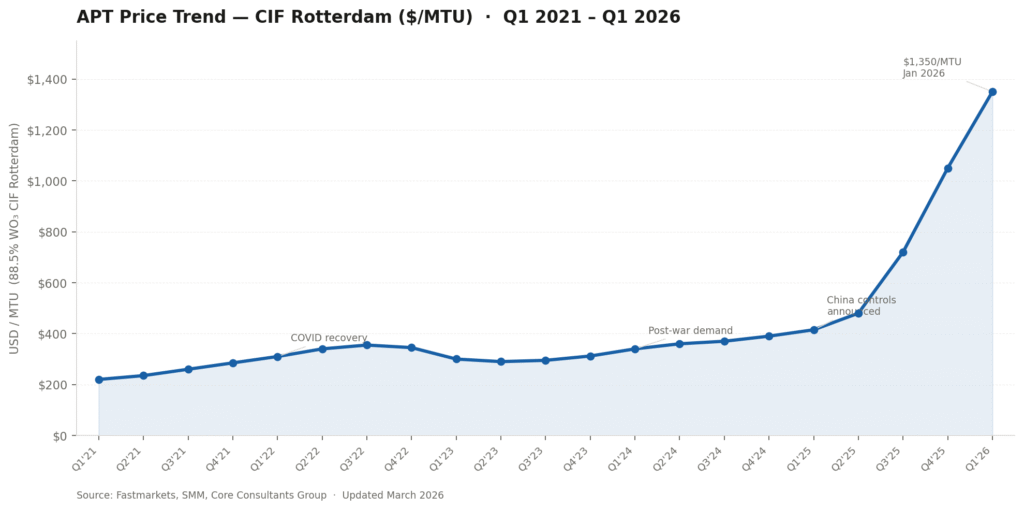

Tungsten pricing has undergone a historic structural shift. Prices across all tungsten intermediates — concentrates, APT, AMT, and powder — have surged dramatically since 2024 on the back of Chinese export controls, defense sector restocking, and surging tech demand.

| Product | 2023 | 2024 | Early 2025 | Jan 2026 | Trend |

|---|---|---|---|---|---|

| APT (CIF Rotterdam, 88.5% WO₃) | $312/MTU | $375/MTU | $415/MTU | $1,350/MTU | ↑ 225% vs 2023 |

| APT (FOB China, 88.5%) | ~$295/MTU | ~$355/MTU | ~$395/MTU | $450+/MTU | ↑ Breaking $450 mark |

| AMT (Ex-works China, ≥81.5% WO₃) | ~$38,000/mt | ~$48,000/mt | ~$58,000/mt | ~$66,928–67,552/mt | ↑ ~76% vs 2023 |

| Ferro-tungsten (≥75%, Rotterdam) | ~$90/kg W | ~$120/kg W | ~$145/kg W | $167/kg W | ↑ +7.4% Jan 2026 |

| Tungsten ore concentrates (FOB Africa) | ~$8,000/MTU | ~$12,000/MTU | ~$16,000/MTU | $22,000–24,000/MTU | ↑ +108% (180-day) |

| Tungsten powder | ~$20,000/t | ~$32,000/t | ~$42,000/t | ~$55,000/t | ↑ 500%+ vs 2024 lows |

Sources: Shanghai Metal Market (SMM), Fastmarkets, Core Consultants Group, GOLDINVEST (March 2026). MTU = metric ton unit (1% of 1 metric ton).

Analyst forecast (2026): Market watchers are eyeing APT breaking $460/MTU in 2026, with forecasts suggesting $400–$450/MTU will become the new structural floor in coming years. CICC projects a global tungsten deficit of 20,000 MTU by 2028 as demand from defense, semiconductors, EV batteries, and AI data centers explodes.

Global Supply Chain & Production Leaders

Understanding where AMT comes from — and the concentration risks embedded in the supply chain — is critical for any procurement or risk management function.

The Geopolitical Situation — March 2026

This is the context most AMT and APT industry resources fail to cover — yet it is arguably the most important factor shaping the market as of the date of this article.

Critical supply alert — March 2026Tungsten prices have surged fivefold over the past year. Chinese exports of some tungsten intermediates — including APT — fell to zero in late 2025 following Beijing’s export control implementation in December 2024. AMT availability in Western markets is severely constrained.

In February 2025, China introduced export controls on tungsten and several other rare metals, reshaping global trade patterns and significantly limiting the availability of intermediate tungsten products. China has historically prohibited the export of tungsten concentrates — preferring instead to export value-added intermediates like APT, AMT, and tungsten oxides — giving it extraordinary leverage over global pricing.

The US Department of Defense classifies tungsten as a critical defense material. Europe is pushing hard for supply diversification. Key alternative supply projects now under active development include Almonty’s Sangdong mine (South Korea, targeting ~7% of global supply), EQ Resources’ Mt. Carbine (Australia), and Guardian Metal Resources’ Pilot Mountain (USA).

AMT vs APT — Side-by-Side Comparison

AMT and APT are frequently confused. They are not the same compound and serve fundamentally different industrial purposes.

Full detailed comparison with interactive charts → Read our complete AMT vs APT guide [LINK]

Frequently Asked Questions

Read Related Topics

Check Scrap Prices

AMT stands for Ammonium Metatungstate. The full chemical name is Ammonium Metatungstate hydrate, with formula (NH₄)₆H₂W₁₂O₄₀·xH₂O. It is also sometimes referenced by its CAS number 12028-48-7.

AMT is predominantly used in catalyst production, accounting for approximately 44% of demand — particularly in petroleum refining for hydrodesulfurization and hydrocracking. It is also widely used in electronics/semiconductors (26%), smart glass electrochromic coatings, DeNOx emission control catalysts, and emerging energy storage applications.

Yes. APT (Ammonium Paratungstate) is the primary raw material for producing AMT. The manufacturing process involves roasting APT, then digesting, filtering, evaporating, and spray drying to yield the final AMT crystalline powder. APT is essentially the upstream precursor that becomes AMT through further refinement.

As of the latest available data (November 2025, Shanghai Metal Market), AMT ex-works China was trading at approximately $66,928–$67,552 USD per metric ton (VAT included: ~$75,628/mt). Prices have risen significantly in 2026 due to Chinese export controls. The benchmark APT price (CIF Rotterdam) reached $1,350/MTU in January 2026, up from $415/MTU in early 2025.

AMT requires additional processing steps beyond APT production (roasting, digesting, filtering, evaporation, spray drying), achieves higher purity levels, and commands premium pricing due to its specialized high-performance applications in catalysts, electronics, and precision coatings. Its significantly higher water solubility (35× APT) makes it uniquely suited for applications where APT cannot be substituted.

China’s December 2024 export restrictions dramatically tightened global supply. By late 2025, Chinese APT exports had fallen to near zero, with AMT availability in Western markets severely constrained. Tungsten prices surged 5× over the past year. The US Department of Defense and European defense sector have responded by securing long-term supply agreements with non-Chinese producers and investing in new domestic projects.

China dominates global production, accounting for approximately 82% of global tungsten concentrate output, with multiple facilities exceeding 10,000 metric tons per year of AMT. However, China’s 2024–2025 export restrictions are accelerating investment in non-Chinese AMT production in Vietnam (Masan), Europe (H.C. Starck), and the United States (Global Tungsten & Powders, Ereztech).

Found this guide useful?

Sources: MarketsandMarkets (Feb 2026), Congruence Market Insights, Shanghai Metal Market (SMM), Fastmarkets, Core Consultants Group (May 2025), Buffalo Tungsten (Dec 2025), GOLDINVEST (Mar 2026), Asian Metal, Chinatungsten Online, Stanford Advanced Materials, ACS Publications. All prices as of dates indicated — tungsten markets are highly volatile in 2026.